By Shaunak Handa, Tushar Gupta

In 301 A.D., the Roman emperor Diocletian issued one of the most extraordinary economic decrees in ancient history: the Edict on Maximum Prices. This law imposed strict price ceilings on more than 900 goods and services (Prodromidis 2006) and threatened severe punishment, including death, for anyone who sold above these limits. Even a Roman elementary teacher who charged more than fifty denarii per pupil each month could face extreme penalties. Such measures raise a striking question: how did the most powerful empire of the ancient world reach a point where the state threatened its own citizens over the price of everyday goods?

By the early fourth century, the Roman economy was experiencing severe inflation and fiscal instability. Rising military expenditures, political turmoil, and the gradual debasement of Roman coinage placed immense pressure on the imperial monetary system. This blog explores where this inflation came from, how it affected citizens, and whether this crisis contributed to weakening the foundations of the Roman Empire itself.

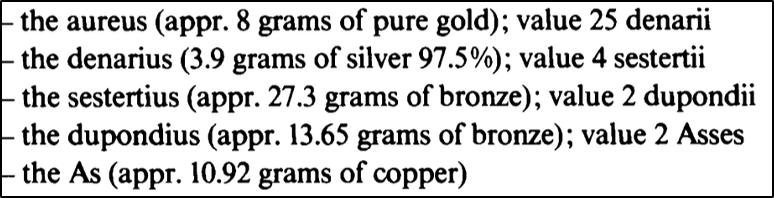

Before answering these questions, it is necessary to examine Roman coinage and why it was central to imperial power. After centuries of a fragmented monetary system, Emperor Augustus established a unified and stable currency around 23 B.C (Wassink 1991). This reform standardized coinage across the Roman Empire and fixed the relationships between gold, silver, and other base metals. Augustus formalized the gold aureus, defined as 1/42 of a Roman pound, and the silver denarius, defined as 1/84 of a pound. Together they formed a bimetallic system in which one aureus equaled twenty-five denarii, while brass and copper coins were introduced for everyday transactions. The structure of this monetary system is illustrated in Exhibit 1.

This standardized currency became the backbone of the Roman economy at the time. In practical terms, coinage helped enable three core functions of the imperial state: paying the army, collecting taxes, and facilitating trade across the empire’s vast territory. This coinage served similar functions to that of modern day money. A reliable currency assisted in maintaining the loyalty of soldiers, allowed provinces to meet tax obligations, and supported long-distance commerce within the Roman economic network.

However, the system contained an important institutional weakness. Authority over coinage rested entirely with the emperor, and an absence of independent institutions to regulate monetary policy or restrict the minting of currency. While the system created stability under competent rulers, it also meant that poor fiscal decisions by emperors could destabilize the entire monetary system.

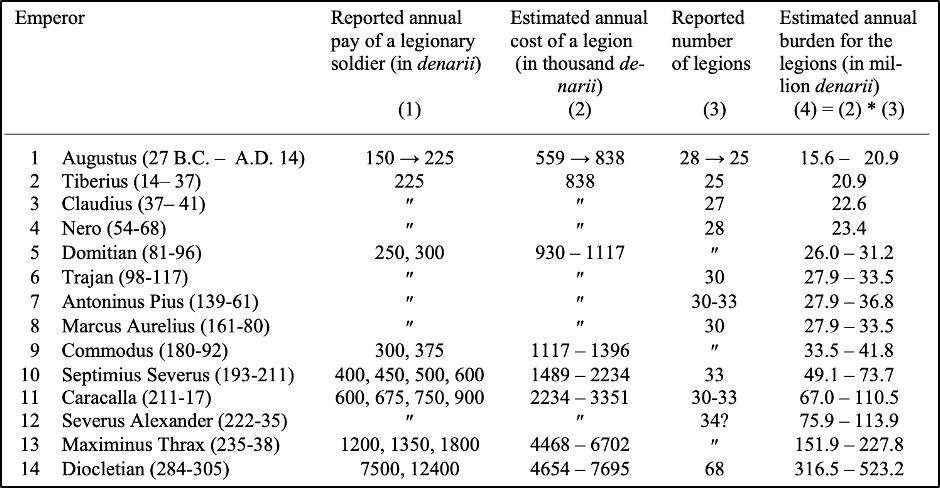

With this structure in mind, we can begin examining the evidence that inflation developed within the Roman economy between Augustus’ monetary reform and Diocletian’s price edict in 301 A.D. One important indicator comes from the empire’s fiscal structure with military spending representing the largest expenditure of the Roman state, consuming approximately one-half to two-thirds of total annual revenue. Exhibit 2 below illustrates this fiscal pressure more clearly. While the estimated number of Roman legions remained relatively stable throughout the first two centuries of the empire, the total annual expenditure on legionary salaries increased steadily over time and rose sharply during the third century. In other words, the Roman state was paying roughly the same number of soldiers, but at significantly higher cost. This rapid increase in military spending placed growing pressure on imperial finances and forced emperors to search for new ways to fund the army, shaping Roman monetary policy in the centuries leading up to Diocletian’s reforms.

Where Did Roman Inflation Come From?

If rising military expenditures strained imperial finances, the next question becomes how Roman emperors chose to fund these obligations. One increasingly common view was coin debasement. Rather than dramatically increasing taxation, emperors reduced the precious metal content of coins while maintaining their nominal value. By minting coins with less silver but the same face value, the state could effectively expand the money supply and finance its growing fiscal commitments.

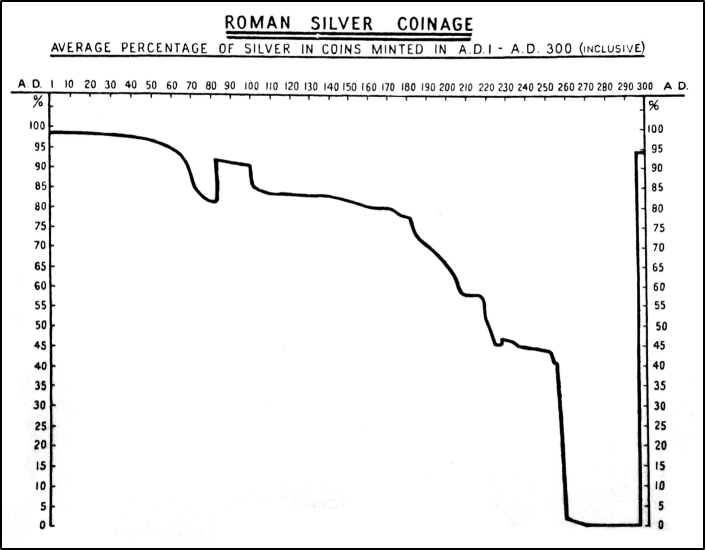

Surviving Roman coins provide strong evidence with numismatic studies measuring both the weight and silver purity of denarii showing a clear decline in silver content over time (Haines 1941). Early imperial denarii were composed of nearly pure silver, but by the third century the proportion of precious metal had fallen dramatically. The historian A. H. M. Jones argues that this debasement was the primary driver of inflation in the Roman Empire. According to Jones, the Roman state relied increasingly on lowering the silver content of coinage in order to meet rising military expenditures, particularly during the politically unstable third century. As more debased coins entered circulation, the purchasing power of the currency declined and prices began to rise accordingly (Jones 1953).

However, other scholars caution against viewing debasement as the sole explanation for Roman inflation. Alfred Wassink argues that the inflationary process was more gradual and structurally complex. While debasement undoubtedly occurred, Wassink suggests that price increases accelerated mainly during the third-century crisis, when political instability, civil wars, and disruptions to trade networks placed additional stress on the Roman economy. In this interpretation, debasement interacted with broader structural pressures rather than acting as a single dominant cause of inflation (Wassink 1991).

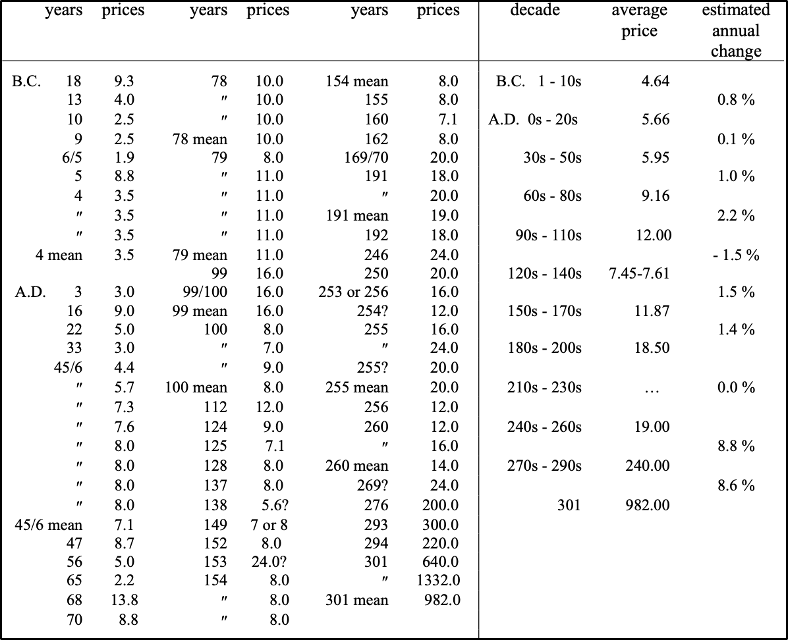

Evidence from commodity prices supports this more nuanced interpretation. Records preserved in Egyptian papyri, shown in Exhibit 3, indicate that wheat prices remained relatively stable for nearly two centuries after Augustus’ monetary reforms. Only during the later third century do prices begin to rise sharply. Prodromidis similarly argues that Roman inflation should be understood as the by-product of both monetary expansion and structural economic pressures, including fiscal instability and administrative costs associated with governing a vast empire (Prodromidis 2006). Taken together, the historical evidence suggests that Roman inflation emerged from the interaction of several forces, not as the conclusion of one policy. While it remains clear that forces such as monetary debasement, rising state expenditures, and the political instability of the third century contributed to inflation, it is frivolous to crown or discount one particular force as the key driver of inflation in the Roman empire.

How Did Inflation Affect Roman Citizens?

The consequences of rising prices were felt throughout Roman society. As the purchasing power of coinage declined, wages struggled to keep pace with the cost of essential goods. Soldiers, merchants, and urban consumers all experienced the effects of inflation in different ways. While emperors periodically increased military salaries, these increases often lagged behind price growth, meaning that real purchasing power could still fall even when nominal pay rose. This dynamic remains a central concern in modern economics: wage adjustments often lag behind inflation, meaning that even when nominal incomes rise, workers may experience a decline in real purchasing power as prices increase faster than wages.

The best way to analyse this is through data from that time period itself. As such, we emanate this effect by the primary source of Diocletian’s Price Edict. The language of Diocletian’s Edict on Maximum Prices reveals how serious the situation had become by the early fourth century. The preamble to the edict claims that merchants were charging “excessive prices” and exploiting shortages to the detriment of ordinary citizens and soldiers. The document frames the policy as a moral intervention, portraying the state as defending the public from greed and speculation.

In response, the edict imposed maximum prices on more than 900 goods and services, ranging from food and clothing to transportation costs and wages for different professions. Violating these price limits carried extremely harsh penalties, including death in certain cases. These extreme measures suggest that the Roman government perceived inflation not only as an economic issue but also as a threat to social order and military stability.

However, the policy illustrates the limitations of state intervention in complex economic systems. Historical evidence suggests that merchants frequently refused to sell goods at the mandated prices, leading to shortages and the emergence of black markets. Instead of stabilizing the economy, the edict may have disrupted trade and further undermined market confidence. When viewed through the lens of later economic thought, particularly Adam Smith’s ideas on market coordination, this episode raises an important question: to what extent can state-imposed price controls override the natural forces of supply and demand without producing unintended consequences (Smith 1776)?

Did Inflation Contribute to the Weakening of the Roman Empire?

The final question remains whether inflation itself contributed to the weakening of the Roman imperial power. Historians have disagreed on the extent of this relationship. Jones views inflation as an important indicator of deeper fiscal instability within the Roman state. In his interpretation, the reliance on coin debasement reflected the government’s growing inability to finance military expenditures through taxation alone. As currency quality deteriorated, confidence in Roman coinage weakened, complicating trade and tax collection across the empire (Jones 1953).

Wassink, however, warns against attributing the empire’s difficulties solely to inflation. While rising prices certainly created economic hardship, he argues that they were only one element within a broader political and military crisis. The third century was marked by frequent changes of emperor, civil conflict, and external invasions, all of which placed enormous strain on imperial institutions. Inflation therefore acted less as a single cause of decline and more as a symptom of deeper structural pressures within the Roman state (Wassink 1991).

What the evidence ultimately reveals is that the Roman monetary system, once a source of imperial strength, became increasingly fragile when confronted with sustained fiscal pressures. The attempt to impose strict price controls in 301 A.D. illustrates both the scale of the economic crisis and the limits of imperial authority in regulating markets. Diocletian’s edict did not eliminate inflation, but it remains one of the most striking historical examples of a state attempting to control prices in response to monetary instability.

The evidence predominantly suggests that inflation in the Roman Empire emerged from the interaction of several structural pressures rather than a single policy failure. Numismatic evidence showing the declining silver content of Roman coins supports the view that monetary debasement contributed to rising prices. However, as Wassink and Prodromidis argue, inflation accelerated primarily during the third-century crisis, when political instability, fiscal pressures, and disruptions to trade tended to place additional stress on the Roman economy.

To Roman citizens, as prices increased, wages often failed to keep pace, reducing real purchasing power and contributing to economic instability. Diocletian’s Edict on Maximum Prices further demonstrates how seriously the Roman state perceived this crisis, attempting to impose strict price ceilings (before being called price ceilings) across the economy. Yet the policy also illustrates the limits of state intervention in markets. Rather than solving inflation, price controls created market distortions.

From an economic perspective, the Roman case highlights how monetary instability can emerge when fiscal pressures, political instability, and weak institutional constraints interact. While it is unfair to judge inflation alone as the decline of the Roman Empire, it exposed underlying weaknesses in the imperial system and revealed the limits of state control over complex economic forces.

References

Cochrane, John H. “Diocletian v. Harris, Part 2: Price Controls.” The Grumpy Economist. August 15, 2024. Diocletian v. Harris Part 2, Price Controls.

DeAgostini/Getty Images. Fresco depicting the baker’s shop, Pompeii. 1st century CE. Fresco. Naples: Museo Archeologico Nazionale. Photograph. https://www.mediastorehouse.com/uig/art/archeology/ancient-roman-fresco-donation-bread-1st-century-9517517.html.

Haines, G. C. “The Decline and Fall of the Monetary System of Augustus.” The Numismatic Chronicle, 6th ser., 1 (1941): 17–47.

Jones, A. H. M. Inflation and the Decline of the Roman Empire. Oxford: Blackwell, 1953.

Prodromidis, Prodromos. “Inflation and the Roman Monetary System.” Journal of European Economic History 38, no. 3 (2006).

Smith, Adam. 1776. An Inquiry into the Nature and Causes of the Wealth of Nations.

Wassink, Alfred. “Inflation and Financial Policy under the Roman Empire to the Price Edict of 301 A.D.” Historia 40, no. 4 (1991).

Leave a comment