By Nicolas Stathopoulos

The Gold Standard was a monetary system that drove Canadian economics for over five decades, well prior to the country we know and see today. Although Canada was officially confederated in 1867, the Gold Standard was introduced in 1854, meaning that monetary policy in Canada was extremely influential in the country’s development over decades of economic fluctuations. This blog post will explore the concept of a gold standard as a monetary policy and analyze its impact on the Canadian economy over the course of time.

Prior to examining the Gold Standard, a background in the benefits of metals used as a means of value can provide some context for the reasoning behind why gold played a pivotal role in the economy. Precious metals allow for a standardized way for individuals to exchange goods in an efficient manner (Celerier, 2026). It allowed for two parties to directly trade with each other, although not necessarily benefiting from each other’s goods, solving the double coincidence of wants (Celerier, 2026). Historically, silver was the key metal commonly exchanged, but gold became the definitive metal of choice due to Isaac Newton, the leader of the Mint of England in 1717, who artificially set the price of silver beyond its demand, and caused a consumer shift to gold (Weber, 2015).

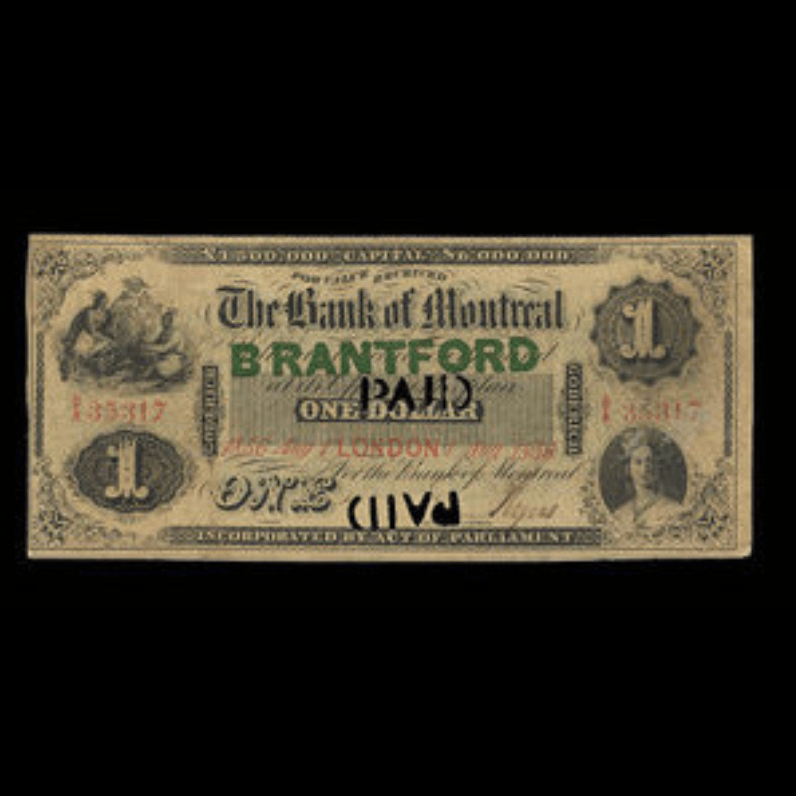

As for the gold standard itself, it is a monetary system in which any currency circulated in the economy can be exchanged for a fixed amount of gold at any point. Banks store reserves of gold and issue notes that are free to use in circulation, but can be redeemed by their users for the equivalent value in gold. An example of a banknote can be seen in Figure 1, from the Bank of Canada. This note specifies it was only redeemable for gold at the Bank of Montreal, unlike currency today, which is free to deposit within any bank across the nation.

Prior to its application to the Canadian economy, the Gold Standard itself originated in Europe in 1821. At the time, the Bank of England officially adopted the Gold Standard across their economy in an attempt to restore stability throughout the nation, following high levels of inflation directly after the Napoleonic Wars (Weber, 2015). Canada, a much smaller economy than England at the time, adopted the Gold Standard on August 1st, 1854, and the benefit to them came in two primary forms.

First of all, by having a common underlying asset-backed currency with larger economies such as England and the United States (which also adopted the Gold Standard around the same

era), Canada faced fewer barriers to trade internationally, and was able to access larger markets than prior to the Gold Standard. As a reference, a Bank of Canada study shows that the average standard deviation of the Canadian dollar relative to the American dollar was 0.104 percentage points over the years 1875 to 1913 (Weber, 2015). This is quite the opposite relative to exchange rates in fiat economies like those today. The population engaged in trade across borders, unlike today, where participants must account for political factors influencing exchange rates.

In addition to economic growth, the Gold Standard provided domestic price stability to Canadians throughout its use. From 1880 to 1914, Canadians experienced an average inflation rate of 0.1% annually (Bordo, 2008). Price stability benefitted the population at the time as it allowed for longer-term projects to be completed with certainty and ensured that the purchasing power for Canadians would remain relatively constant across time.

Although beneficial throughout many years in Canada during economic stability, there was certainly scepticism surrounding the potential flaws within a gold-backed monetary system. Critics argued that a monetary system that is backed by gold is not flexible during times of crisis, but rather proves relatively ineffective relative to a fiat system (Powell, 2005). The start of World War 1 proved to be an extremely vulnerable period for the Gold Standard, as predicted. Prior to the war, Canadian banks saw a large number of people attempt to withdraw their deposits in the form of gold due to the ongoing uncertainty, which was ultimately the first sign of changes to come (Iddon, 2025).

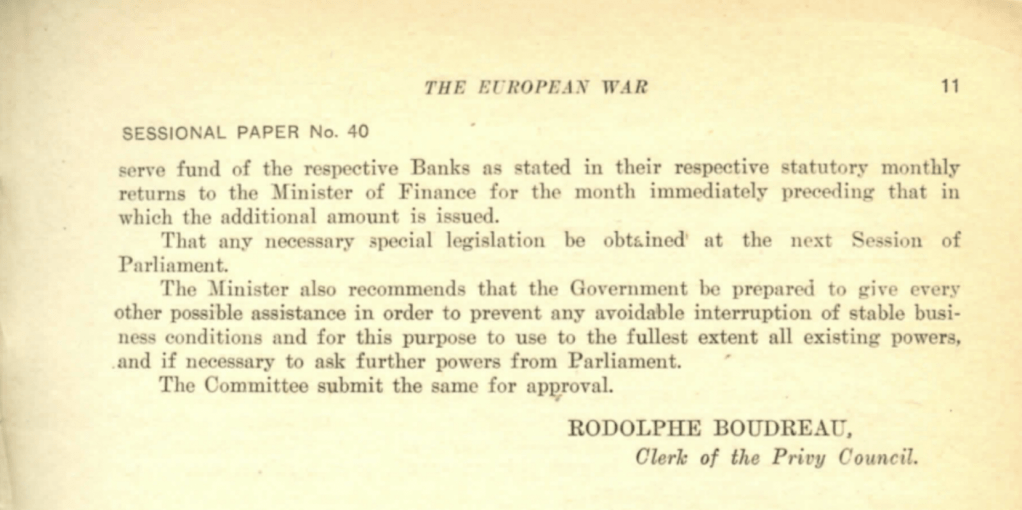

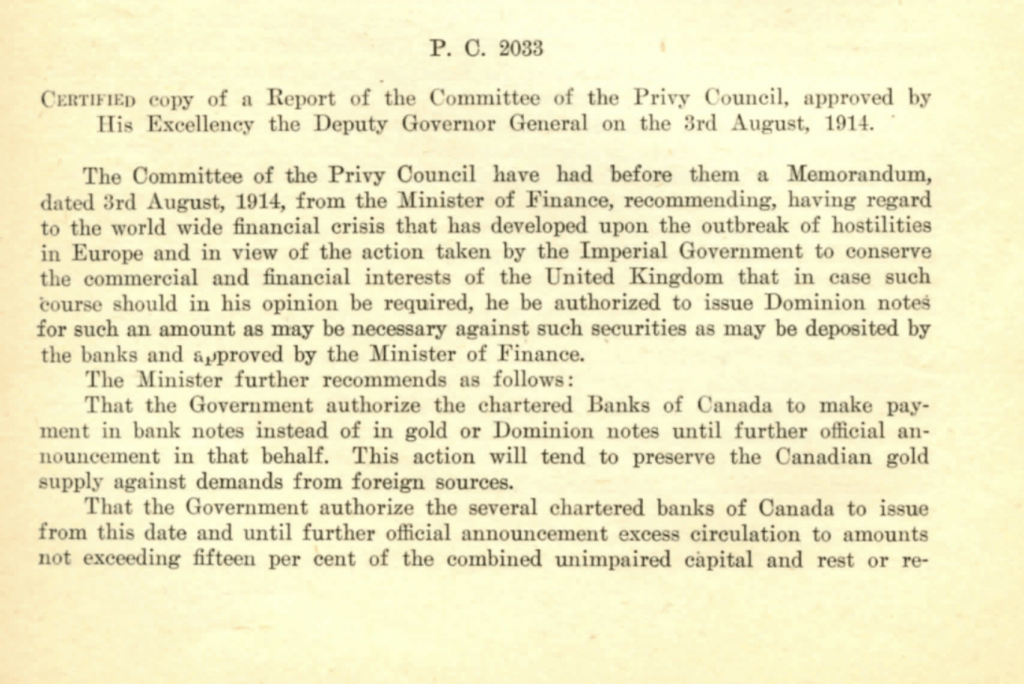

The Bank of Canada highlighted the primary reason that a gold standard was simply impossible to uphold during times of War (Iddon, 2025). When governments needed to raise funds for the war, the central bank would be unable to provide them with sufficient funds, unless it simultaneously increased its gold reserve supply (Iddon, 2025). This meant that participating in the war would mean abolishing the monetary system that backed the Canadian economy for five decades. The abolishment of the Gold Standard was recommended in 1914 (Powell, 2005). A governmental council report from the time highlights the recommendation from the Minister at the time. The segment of the report is highlighted in Figure 2 (Canada, 1914). It was recommended that banks could pay their depositors in banknotes as opposed to gold, marking the end of the Gold Standard (Canada, 1914). The Gold Standard was ultimately abandoned in that same year, following the start of World War 1. It shortly returned following the end of the war, but suspension of gold convertibility ultimately occurred in 1929 due to further economic difficulties linked to the Great Depression. What was once an advantageous benefit of the Gold Standard turned out to be an extremely limiting constraint. The structure was mechanically inefficient in times of war.

In conclusion, the Gold Standard proved to play an important factor in Canadian History, but was extremely unsustainable over extended periods of time. This gold-backed monetary system posed significant threats during difficult economic moments, and truly only thrived in consistent economic conditions. The Gold Standard will remain a crucial moment of Canadian history, as it shaped the monetary system we see today. It highlights the need for a flexible monetary system in times of uncertainty and the impacts that shocks can have on society.

References:

Bordo, M. D. (2008, April 14). Gold standard. Econlib. https://www.econlib.org/library/Enc/GoldStandard.html

Celerier, C. (2026, January 22). Slides: Slides_China_PaperMoney_2026.pdf [Lecture slides]. University of Toronto.

Collections. (n.d.). Bank of Montreal, 1 dollar, August 1, 1856. Bank of Canada Museum. https://www.bankofcanadamuseum.ca/collection/artefact/view/1967.0128.00011.000/canada-bank-of-montreal-1-dollar-august-1-1856

European War. (n.d.). Documents of the European War. Wartime Canada. https://wartimecanada.ca/sites/default/files/documents/Documents%20of%20the%20European%20War.pdf

Iddon, G. (2025, August 5). Good as gold? A simple explanation of the gold standard. Bank of Canada Museum. https://www.bankofcanadamuseum.ca/2025/08/good-as-gold-a-simple-explanation-of-the-gold-standard/

Powell, J. (2005, December). A history of the Canadian dollar. Bank of Canada. https://www.bankofcanada.ca/wp-content/uploads/2010/07/dollar_book.pdf

Weber, W. E. (n.d.). A bitcoin standard: Lessons from the gold standard. Bank of Canada. https://www.bankofcanada.ca/wp-content/uploads/2015/12/bitcoin-standard-lessons.pdf

Leave a comment