By Fallyn Harper, Martina Mesic, Shabdhaki Rasalingam

Introduction

In the 19th century, railroads were considered a revolutionary way of transportation, significantly reducing travel time and costs. Aside from travel, railroads expanded trade by connecting different markets across the country. This new form of transportation became very popular, and many believed it would reshape the economy. Despite the clear economic benefit of railroads, the massive expansion of railway networks triggered huge speculation and financial instability across the world, especially in Britain and the United States. Overconfident investors poured large amounts of capital into railway companies, only for many of the projects to turn out to be unprofitable, overvalued or, unfinished. This situation begs the question: if railroads were truly the way to transform the economy, why did so many investors lose their fortunes during railway speculation?

How a Bubble Forms

To understand why this massive speculation occurred, we must first understand how bubbles form in the first place. When a new technology emerges, investors get excited and want to invest capital into this opportunity. Its popularity increases due to widespread media coverage creating a “fear of missing out” amongst the public. Many are drawn to the market and share prices will continue to rise far beyond their fair value. Some experienced investors may be able to see the warning signs of a bubble, but it is very hard to guess exactly when a bubble will burst. Eventually, a small event can burst the bubble, causing panic and leading to a massive market crash (Segal, 2025). The 19th century railroad expansion followed many of these same dynamics.

British Railway Mania

The British railway mania has been described as one of the greatest technological revolutions and financial crises in history (Odlzyko, 2010). It began in 1825 when the Stockton and Darlington railway opened to transport coal from the Durham coal mines to the Stockton-on-Tees port. (Heritage Calling, 2025). By 1830, the Liverpool and Manchester Railway opened, becoming the first inter-city railway to transport passengers using only steam locomotives (Railway200, n.d). Railroads transformed the way people traveled and traded. Investors saw this transformative technology as an opportunity to tap into an untouched market with high revenue projections. This opportunity resulted in the Great Railway Mania of the 1840s.

It’s helpful to consider the economic environment during this time. The Bank of England cut interest rates in the early 1840s which decreased borrowing costs for investors. An increase in trade and the ongoing industrial revolution expanded the British middle class, creating a large group of people that railroad companies could aggressively market to. By 1845, about half of newspaper ads were for railways, some with misleading claims about revenue growth and risk (Reynolds, 2025).

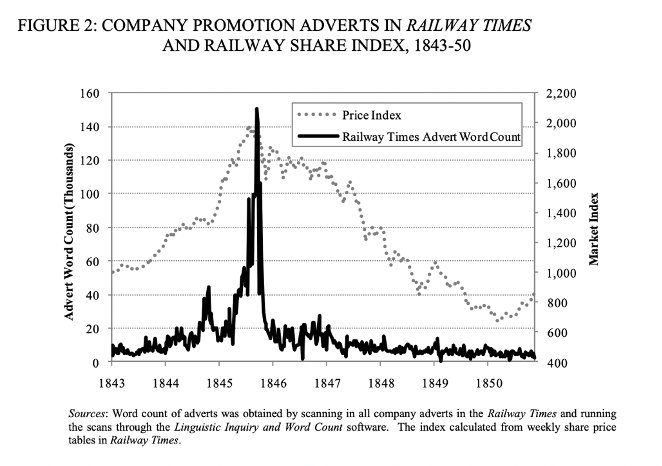

To attract more investors, stocks were allowed to be bought on margin requiring only a 10% deposit of total value. This environment drastically increased the number of investors in the market and the number of railway securities listed on London Stock Exchange, with some stock prices almost tripling. Figure 1 shows the positive correlation between stock prices and promotion adverts during the Railway Mania.

Some companies committed actual crimes to maintain the hype. For example, George Hudson, nicknamed “the railroad king”, owned over 1,000 miles worth of railway track and was caught for fraudulent financing practices. The Belfast Newsletter from April 13, 1849, lists the many crimes of Hudson, which include keeping financial transactions off company books, purposely selling shares above market value, charging excessive brokerage fees, and misusing company capital for his own benefit (Belfast News-Letter, 1849). He also was caught paying out dividends from the company’s capital rather than profits to keep share prices high (Reynolds, 2025).

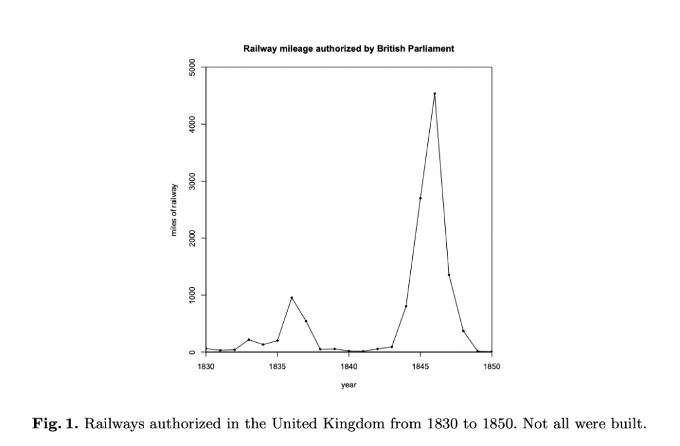

The British government had a “laissez-faire” approach during the railway expansion. There were 44 committees responsible for approving projects and in 1845, every single committee approved at least one project while only a minority being rejected (Campbell, 2014). At its peak, Parliament passed 272 Acts for new railway companies and there was 9,500 miles of track projected to be built (Husain, 2019). Figure 2 shows railway mileage authorized by Parliament throughout the mania.

Overall, the low-interest rate environment, misleading advertisements to a growing middle class, a laissez-faire government, and hungry investors plagued with irrational exuberance caused stock prices to continually rise far beyond what was sustainable. Eventually, the Bank of England raised interest rates, greatly affecting the highly leveraged positions companies and investors were in. By 1850, stock prices had fallen 57.5% from peak to trough (Campbell, 2014) with total capital invested in the railway industry representing almost half of total GDP (Odlyzko, 2010). This railway expansion was an international phenomenon, affecting many nations including the United States.

Railway Mania in the United States

The speculative dynamics observed during Britain’s railway boom also appeared in the United States as railroad technology spread across the Atlantic. During the nineteenth century, railroads were seen as the infrastructure that would connect distant markets and support national economic growth. As a result, investors and governments treated railroad construction as a strategic economic priority. Railroad development in the United States expanded rapidly during the mid-nineteenth century. Railroads first appeared in the 1830s and by 1840, more than 2,800 miles of track were in operation across the country. The railway network had expanded to over 9,000 miles in 1850 (Association of American Railroads, n.d). Railroad construction continued to increase after the Civil War.

Government policy played a central role in enabling this expansion. The federal government granted large tracts of land to railroad companies across the western United States. These land grants transferred millions of acres to private firms, who could sell the land to settlers or pledge it as collateral when issuing bonds to investors. This policy aimed to promote settlement and infrastructure development, but it also encouraged companies to expand rapidly even when projected revenues were uncertain.

Railroad construction required substantial capital, which companies raised primarily through debt markets. Domestic and foreign investors, including British and Dutch investors, purchased railroad bonds based on expectations that railroads would generate future profits as trade and migration expanded westward. Railroad investment eventually represented ~6% of U.S. GDP (Olaughlin, 2023). Financial institutions played an important role in facilitating these investments by marketing railroad securities to investors.

One of the most prominent financiers was Jay Cooke & Co., a banking firm that had gained popularity by marketing U.S. government bonds during the Civil War. By the late 1860s the firm became heavily involved in financing the Northern Pacific Railway, a project intended to connect Duluth on Lake Superior with Seattle (Koerting, 2023). The project relied on short-term financing to fund long-term infrastructure construction, creating significant liquidity risk if investors withdrew funding.

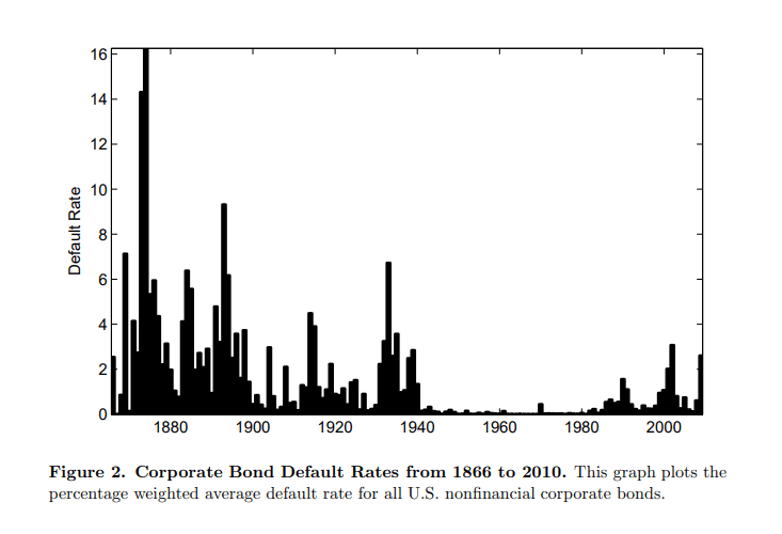

The scale of financial instability is reflected in corporate bond default data. As shown in Figure 3, corporate bond default rates increased during the decades following the Civil War. More than 50% of all outstanding corporate bonds defaulted between 1871 and 1879 as many railroad companies became insolvent after rapid expansion during the post-Civil War infrastructure boom (Giesecke et al., 2012).

Corporate governance failures also contributed to excess speculation. The Credit Mobilier scandal revealed how insiders associated with the Union Pacific Railroad created a separate construction company and awarded it contracts to build the railroads at inflated prices. Since the same insiders controlled both firms, they were able to generate large personal profits through the construction company while transferring the financial burden to the construction company and its investors (Hoopes, 1991).

The speculative expansion of railroad finance contributed to the Panic of 1873, when Jay Cooke & Co. collapsed after failing to raise additional capital for the Northern Pacific Railway. Since banks and investors were heavily exposed to railroad securities, the firm’s failure triggered widespread financial instability and started a long economic downturn known as the Long Depression (Klitgaard & Narron, 2016). The railroad boom reflects a broader pattern in financial markets in which transformative technologies generate large amounts of speculative investments.

Connecting Back to Modern Day

Much like railroads in the 19th century, AI is being viewed as an innovation that is extremely transformative with the potential to reshape many industries. The Magnificent 7 technology stocks, such as Apple, Nvidia, and Alphabet make up around 33% of the S&P500 index fund and contribute greatly to the fund’s volatility. These companies have invested immensely into AI infrastructure over the past couple of years. For example, Alphabet invested $14 billion on capex in the last quarter of 2025, with its spending being heavily focused on AI infrastructure and data centers. Meta is expected to spend $115-$135 billion on AI infrastructure in 2026, which is almost double what they spent in 2025 (The Globe & Mail, 2026). This large increase in investment raises questions about whether the excitement is truly linked to long term economic growth or if it’s the beginning of a speculative bubble. Major technological revolutions often generate financial speculation before it fully integrates into the broader economy (Perez, 2002).

Thinking back to the question posed in the beginning of this post, railroads were a legitimate means of significantly transforming transportation and economic systems, but the financial speculation that stemmed from it caused investors to underestimate the risks of rapid expansion for the benefit of short-term profits. Although new technologies can create real economic progress, they can also lead to dangerous speculation and a large downfall, which is an important lesson for the current market as they manage the rise of AI.

References

Belfast News-Letter. (1849, April 13). Mr. Hudson and the York, Newcastle, and Berwick Railway. The British Newspaper Archive. https://www.britishnewspaperarchive.co.uk/

Campbell, G. (2014). Government policy during the British railway mania and the 1847 commercial crisis. In British Financial Crises since 1825 (pp. 58–75). Oxford University Press. https://doi.org/10.1093/acprof:oso/9780199688661.003.0004

Campbell, G., & Turner, J. D. (2015). Managerial failure in mid-Victorian Britain?: Corporate expansion during a promotion boom. Business History, 57(8), 1248–1276. https://doi.org/10.1080/00076791.2015.1026260

Crisis chronicles: Railway mania, the hungry forties, and the commercial crisis of 1847. (2015, June 5). Liberty Street Economics. https://libertystreeteconomics.newyorkfed.org/2015/06/crisis-chronicles-railway-mania-the-hungry-forties-and-the-commercial-crisis-of-1847/

Giesecke, K., Longstaff, F., Schaefer, S., & Ilya Strebulaev. (2012). Macroeconomic Effects of Corporate Default Crises: A Long-Term Perspective. National Bureau of Economic Research. https://doi.org/10.3386/w17854

Hoopes, R. (1991, February). It Was Bad Last Time Too: The Crédit Mobilier Scandal of 1872. American Heritage. https://www.americanheritage.com/it-was-bad-last-time-too-credit-mobilier-scandal-1872

Husain, T. (2019, September 19). Media and the British Railway Mania of the 1840s. The Property Chronicle. https://www.propertychronicle.com/media-and-the-british-railway-mania-of-the-1840s/

Klitgaard, T., & Narron, J. (2016, February 5). Crisis Chronicles: The Long Depression and the Panic of 1873. Federal Reserve Bank of New York. https://libertystreeteconomics.newyorkfed.org/2016/02/crisis-chronicles-the-long-depression-and-the-panic-of-1873/

Koerting, G. (2023). Panic of 1873. EBSCO. https://www.ebsco.com/research-starters/history/panic-1873

Odlyzko, A. (2010). Collective hallucinations and inefficient markets: The British railway mania of the 1840s. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1537338

OLaughlin, D. (2025, December 17). Lessons from History: The Great Railroad Buildout. Fabricated Knowledge. https://www.fabricatedknowledge.com/p/lessons-from-history-the-great-railroad

Perez, C. (2002). Technological revolutions and financial capital: The dynamics of bubbles and

golden ages. Edward Elgar Publishing.

Reynolds, O. (2025, November 4). Railway mania: the largest speculative bubble you’ve never heard of. FocusEconomics. https://www.focus-economics.com/blog/railway-mania-the-largest-speculative-bubble-you-never-heard-of/

Segal, T. (2025). Understanding the 5 Stages of an Economic Bubble. Investopedia. https://www.investopedia.com/articles/stocks/10/5-steps-of-a-bubble.asp#toc-the-lifecycle-of-an-economic-bubble

Unknown. (2026). Mag 7 AI arms race: Heavy capex, FCF strain and one clear winner. The Globe and Mail. Retrieved March 16, 2026, from https://www.theglobeandmail.com/investing/markets/stocks/TSLA/pressreleases/183716/mag-7-ai-arms-race-heavy-capex-fcf-strain-and-one-clear-winner/

Leave a comment